Flood zone labels can look simple on paper, but they often raise practical questions for homeowners, buyers, and property owners in Greenville, NC.

A certificate of insurance can look like a simple one-page form, but it often plays a major role in contracts, vendor approvals, leases, and project requirements.

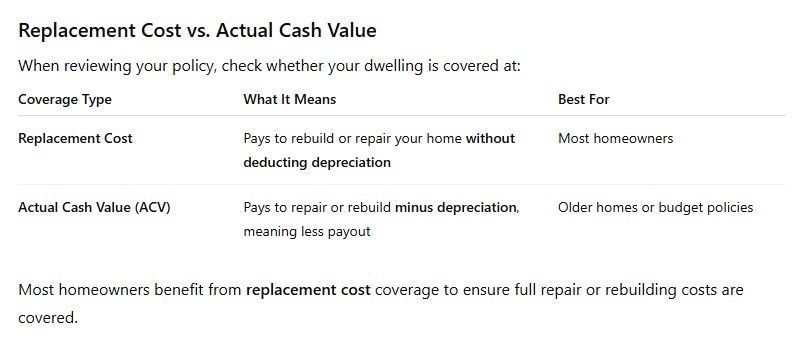

A home insurance claim can feel overwhelming when damage interrupts your routine and you are not sure what happens next. For homeowners in Greenville, NC, understanding the claim process from the first report to the final payment can help you stay organized, avoid delays, and make better decisions during a stressful si

A breakdown rarely happens at a convenient time, and even a simple flat tire can become stressful when you are far from help. For drivers in Greenville, NC, roadside assistance coverage can be a practical add-on that helps reduce uncertainty when a vehicle problem interrupts the day.

Flood damage can be expensive, stressful, and misunderstood, especially when homeowners assume

Business insurance can look complete at first glance, but important gaps may not be obvious until a claim happens.

Home renovations can improve comfort, function, and property value, but they can also change how your home should be insured.

“Full coverage” sounds reassuring, but it can mean different things depending on the policy, vehicle, lender requirements, and coverage choices.

Private flood insurance and NFIP flood insurance both help protect against flood loss, but they are not identical products. The best choice depends on the property

Business interruption insurance helps replace lost income and certain ongoing expenses when a covered event forces your business to slow down or temporarily stop operating